2025 At a Glance:

Many of the forces that reshaped markets in prior years became more pronounced in 2025, with some new twists and turns.

The return of the Trump Administration brought a different policy environment, marked by early and forceful action on trade and immigration. The implementation of these initiatives proved more consequential than markets initially anticipated. The Administration moved decisively on tariffs and border policy, contributing to heightened uncertainty for households and businesses alike, and driving up market volatility.

Financial markets provided early signals that the global economic and financial order may be evolving. Investors witnessed the unusual combination of a weakening U.S. dollar, declining U.S. equity prices and rising Treasury yields. At the same time, capital began moving toward non‑U.S. equities, with several international developed and emerging markets outperforming the U.S., particularly on a non‑USD basis.

Artificial Intelligence remained a powerful market theme with the investment focus broadening beyond a narrow group of mega-cap companies. The scale of required investment continued to draw in complementary sectors, including energy, infrastructure, and credit markets, creating both risks and opportunities.

Private markets remained characterized by conditions that have prevailed since 2022. Exit activity stayed muted, and liquidity constraints continued to delay distributions. Within Private Debt, investors became more focused on whether certain strategies could continue to generate attractive returns in a more challenging market environment.

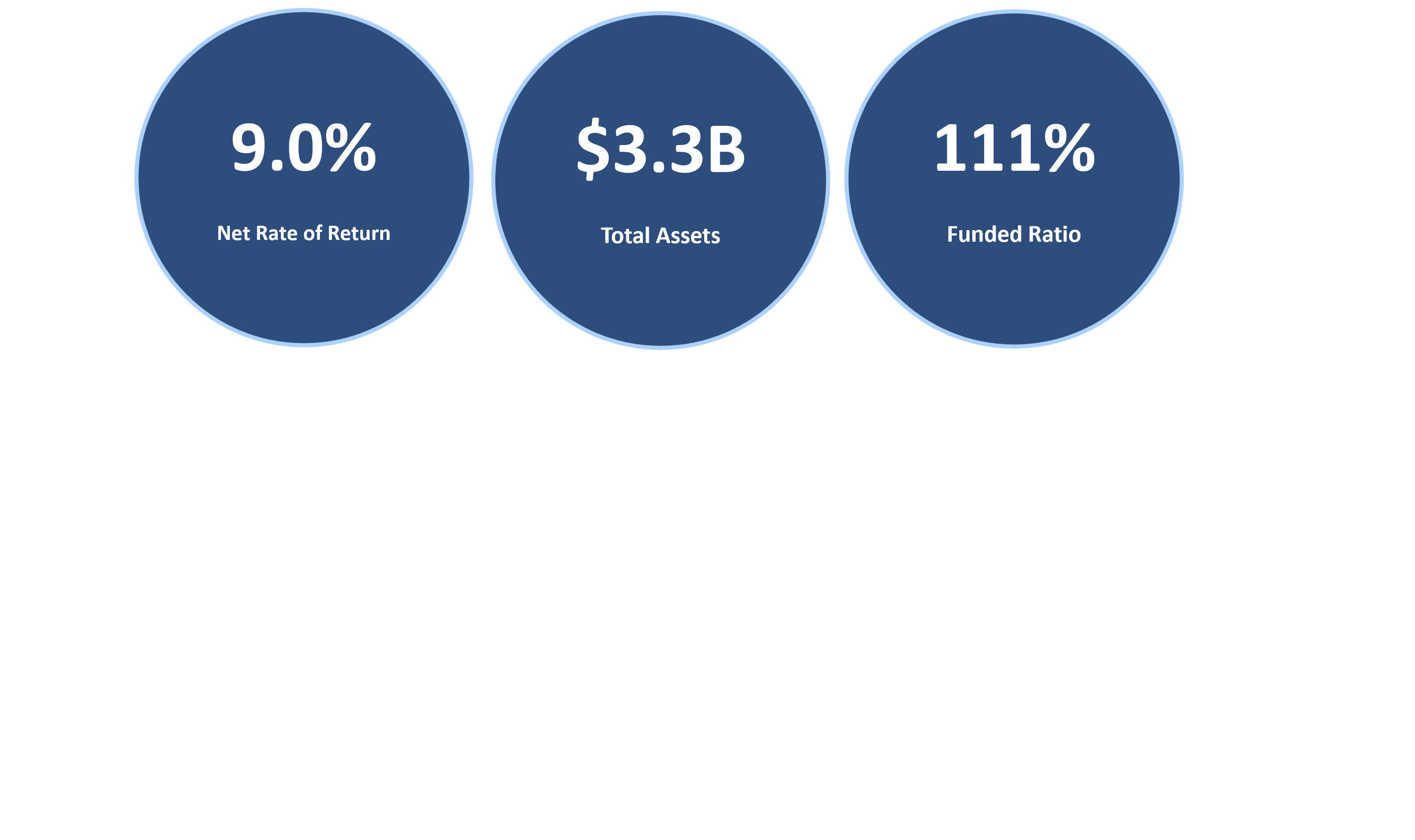

Against this backdrop, the Plan delivered another year of strong absolute results, generating a net return of 9.0%. Performance fell short of the 12.8% benchmark return, with Public Equities modestly underperforming, and Real Assets and Private Equity contributing more meaningfully to the shortfall. The underperformance of Private Equity was consistent with broader industry experience and peer outcomes, as valuation adjustments and limited liquidity continued to weigh on reported returns versus global market cap weighted indices.

Overall, we believe the Plan’s diversified structure proved resilient in a year marked by policy shocks and shifting correlations. Performance compared favorably to Peer Universes, which recorded a median return of 4% to 8%, highlighting the benefits of disciplined portfolio construction and diversification across regions and asset classes.

For more information on our Plan’s assets and investment performance, download our most recent annual report.

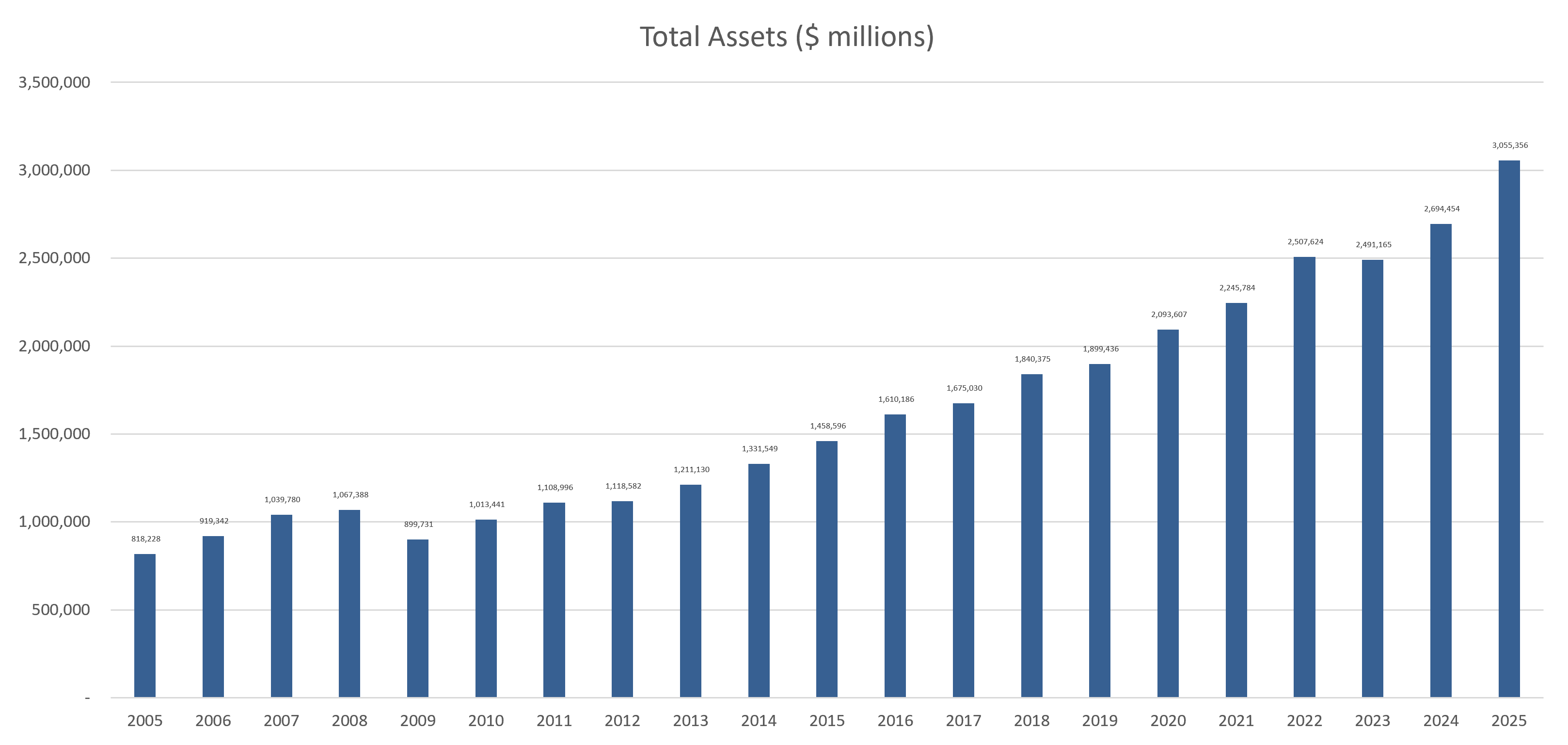

Growth in Net Assets:

Assets continued to grow in 2025 as investment returns and contributions to the Plan exceeded pension payments and Plan-related expenses. Plan assets totaled almost $3.3 billion at the end of 2025. The chart below shows the

growth of Plan assets since 2005.